Then again, it may just be: no income for the banks, they go bust, who will provide banking services to poor people? kind of retarded mental gymnastics.

Credit unions would actually be impacted far more from this legislation than banks.

They don’t have access to the same cash making options that large banks do, and credit unions are also non profit.

If their fee income was reduced, they would have to make up for it in other areas, such as higher lending rates, which affects more people than overdraft fees.

Personally, I’d rather deal with overdraft fees than have a higher rate for loans. If you learn to bank responsibly overdraft fees won’t be an issue anyway.

Overdraft fees simply wouldnt be an issue if they didnt exist. Theres no reason a transaction shouldnt decline if there are insufficient funds. If you dont have the money then you dont have the money.

Theres no reason a transaction shouldnt decline if there are insufficient funds.

I’ll admit I’m ignorant to banking on a large scale, but the few banks I have used and worked for I’ve always had the option to just decline “overdraft protection” so indeed if I tried to make a $50 purchase and I had $45 in my account, it would just decline. Overdrafting has always been an optional service. Are there banks that force you to enable overdrafting?

Edit: now whether the choice is properly conveyed to people is another matter of course, I imagine many banks make it seem like a “good” thing or the default option.

You are correct it is optional but its defaulted to on then you have to listen to their spiel about how good it is for you before being able to turn it off. Even after you do so though it still doesn’t stop some recurring payments or charges so your account can still end in the negative and you typically get a charge for that if its in the negative enough (usually more than 5-10 dollars)

Yes, I agree that their spiels usually make opting out not seem like an option lol.

But I do what to point out this:

Even after you do so though it still doesn’t stop some recurring payments or charges so your account can still end in the negative and you typically get a charge for that if its in the negative enough (usually more than 5-10 dollars)

If you have not agreed to overdraft protection, they legally cannot charge you a fee if you end up overdrafting from automatic payments or another tricky one is gas pumps where some only charge $1 to initiate the pumping then later hard post the full amount. Now, I’m am sure there are institutions that go against this law but I try to spread the word that Reg E doesn’t allow that practice.

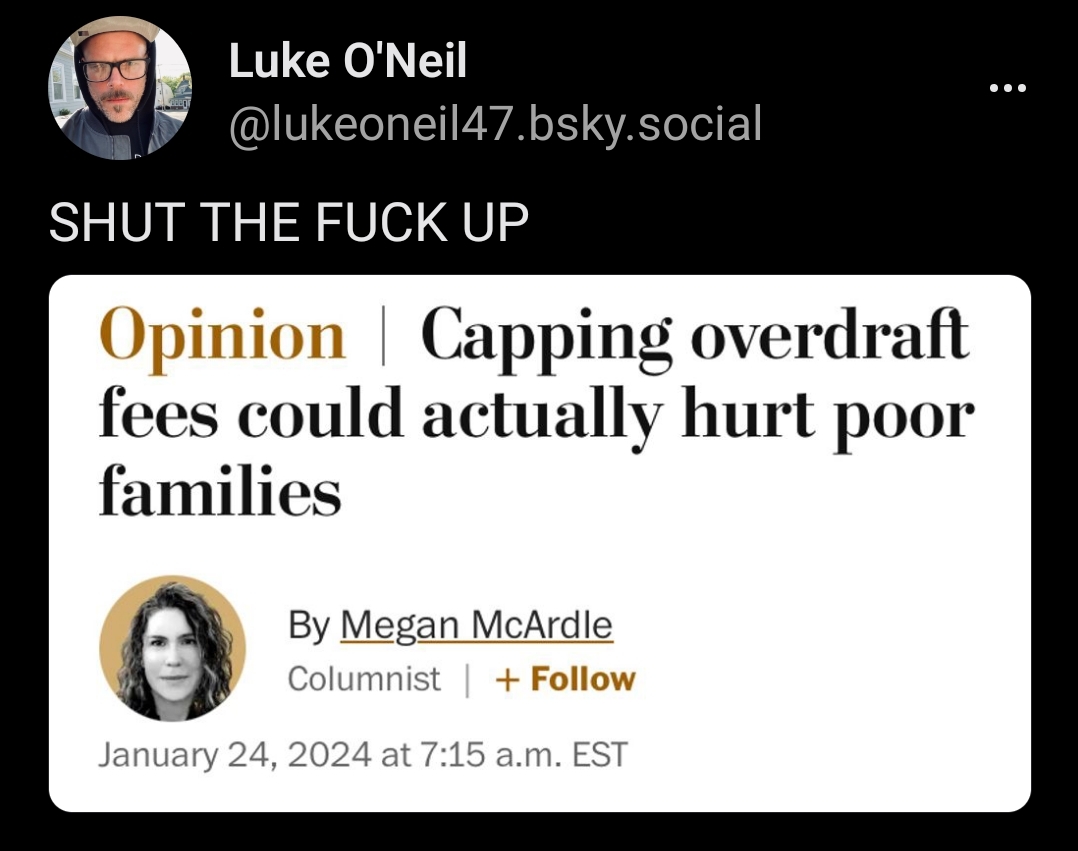

These people are far and away the heaviest users of bank overdrafts. The Financial Health Network, a personal finance nonprofit, says the group most likely to overdraft includes “financially vulnerable” households that struggle to pay their bills every month and typically make less than $30,000 a year. Almost half of financially vulnerable households with checking accounts overdrafted in 2022, and of that group, two-thirds overdrafted at least three times, one-third did so six or more times, and one-fifth overdrafted 10 times or more. With an average overdraft fee of $26.61, hundreds of dollars in fees can land on the most cash-strapped customers. Capping those fees — possibly as low as $3 — would be a huge boon to families who really need the help. Who could oppose that?

Well, as with any nice-sounding policy, it’s important to consider the alternatives, both for the customer and for the banker.

For depositors, overdraft fees can be an expensive alternative to even worse options, such as payday loans or having their electricity shut off (and paying a reconnection fee to turn it back on). And “the best of bad alternatives” can also be sort of true for bankers, who must find some way to defray the cost of providing what is basically an unsecured loan to people who are, as we’ve seen, often financially struggling and might be unable to repay the money. The fees also help pay for “free” checking (which costs banks quite a bit of money to provide).

If we cap overdraft fees, how will banks make up the lost revenue?

From profits, you say, and fair enough, but Patrick McKenzie, who writes the Bits About Money newsletter, points out that the reason your bank is so obsessed with getting you to sign up for paperless statements is that the profit margins on checking accounts are so thin, they can be meaningfully improved by saving the cost of 12 stamps a year. “Margins on small bank accounts are very thin,” he wrote recently, and “credit losses can easily be larger than several years of them.”

Now the government wants to make those accounts even less profitable. It seems possible banks would look to limit their losses by getting rid of those customers or making up the revenue somewhere else — or possibly both. This seems to have happened in the past, judging from what we saw when federal regulators preempted some state fee caps in 2001. According to researchers from the New York Fed, the exempted banks both raised overdraft fees and expanded available overdraft credit, while lowering minimum balance requirements. The rate at which checks were returned for insufficient funds declined by 15 percent. And the share of low-income households with a bank account rose by 10 percent, suggesting that minimum balance requirements had kept those households from opening accounts.

That doesn’t mean that no one would benefit from this rule. High overdraft fees can also deter people from opening a bank account, and it’s possible that effect would outweigh any contraction of credit. The financial industry has also changed a lot since 2001, with nonbank alternatives, such as Cash App, that might offer the marginal bank customer a better replacement than an old-fashioned check-cashing store. But there would still likely be winners and losers, and I don’t know whether the former’s gains would outweigh the latter’s losses. I’m not sure the administration does, either.

it’s only a problem if you see the banks as only a profit source and not as a service.

We had to force corps / government to give us days off, Healthcare, voting, not being slaves, electricity, water, internet… all things they wanted to be products and not services

Yeah, you don’t make a huge amount of money on a service that everyone needs - boo fucking hoo, close the business and get a real job and stop eating avocado toast.

Truly one of the dumbest articles that I have seen.

Having any margin at all on a checking account is just gravy for a bank. It is not their primary source of revenue and never has been. Checking accounts are a mechanism to get customers to do business with them. It’s a marketing/advertising program, that has become required in the industry.

Bank’s are only interested in loans and deposits. This is where banks make the bulk of their money.

When it comes to the poorest people in society, they are not depositing much money or taking out loans. Bankers see them as freeloaders on a system designed to draw in people with more money. They can’t outright deny to service them without a marketing disaster so they punish them instead. Taking money from them to help defray the cost of their marketing efforts. Instead of just denying the charge for insufficient funds as they ethically should, they created an elaborate fee system to bleed money from them.

This is why you should always deny the overdraft protection on any checking account. Never let them charge you a fee for a charge they should have rejected.

I always wonder why it is like a given that they have to make a certain amount each year or else. What would be so bad if they just made a little less?

Their point is that poor people use overdrafting instead of making actual loans. Removing the overdraft revenue from banks would make banks not offer it, making it necessary for poor people to take worse loans.

It’s just an opinion piece and the author admits that it could have other results.

The general concern is if you remove the overdraft fee as a tool, banks will just require a minimum or cancel you.

If financially struggling families can’t even access basic banking, they are further disenfranchised and removed from a stability, and eventually wealth generation

Sounds like a great time to actually bring back postal banking if the “job creators” can’t handle just making “some money” instead of " lots of money" from these accounts.

I’m sure the post office would be glad to have the “some money.”

Well under Obama there was that weird sorta savings account thing they had. I dropped twenty bucks in it just to check it out. They ended the program I think in 2014.

Sounds fine. And unfortunately banks are extremely real job creators. The existence of loaned capital to start business, pay employees and so on are a course of business development.

Ultimately, weather you like them or not, you can’t force a business to work with a given customer, especially if that customer is unreliable or requires more work.

I agree the time of government is to look after people with less/no concern for their profitability, especially when basic well-being and stability are in play.

Yeah you can force a business to work with a customer they don’t want. Go open a restaurant and refuse to serve people based on race, see what happens. We force insurance companies to cover people with massive health problems, companies to make diversity hires, banks to lend money to minorities, buses to take pretty much anyone with a valid ticket, bakers to make gay wedding cakes…

Some how some way the world hasnt collapsed into ruin.

{kind=link}

No, I want to hear the warped logic.

Then again, it may just be: no income for the banks, they go bust, who will provide banking services to poor people? kind of retarded mental gymnastics.

Crux of the argument?

Profit margins are very small on small personal bank accounts. If NSF fees are reduced, how ever will we profit from these tiny accounts?!

https://archive.is/ybfiw

One bank made only 49 billion profit last year, up from 48 billion in 2022. Why won’t somebody think of the banks!?

Oh no, anyways credit unions exist and rarely have these issues

Credit unions would actually be impacted far more from this legislation than banks.

They don’t have access to the same cash making options that large banks do, and credit unions are also non profit.

If their fee income was reduced, they would have to make up for it in other areas, such as higher lending rates, which affects more people than overdraft fees.

Personally, I’d rather deal with overdraft fees than have a higher rate for loans. If you learn to bank responsibly overdraft fees won’t be an issue anyway.

Overdraft fees simply wouldnt be an issue if they didnt exist. Theres no reason a transaction shouldnt decline if there are insufficient funds. If you dont have the money then you dont have the money.

I’ll admit I’m ignorant to banking on a large scale, but the few banks I have used and worked for I’ve always had the option to just decline “overdraft protection” so indeed if I tried to make a $50 purchase and I had $45 in my account, it would just decline. Overdrafting has always been an optional service. Are there banks that force you to enable overdrafting?

Edit: now whether the choice is properly conveyed to people is another matter of course, I imagine many banks make it seem like a “good” thing or the default option.

You are correct it is optional but its defaulted to on then you have to listen to their spiel about how good it is for you before being able to turn it off. Even after you do so though it still doesn’t stop some recurring payments or charges so your account can still end in the negative and you typically get a charge for that if its in the negative enough (usually more than 5-10 dollars)

Yes, I agree that their spiels usually make opting out not seem like an option lol.

But I do what to point out this:

If you have not agreed to overdraft protection, they legally cannot charge you a fee if you end up overdrafting from automatic payments or another tricky one is gas pumps where some only charge $1 to initiate the pumping then later hard post the full amount. Now, I’m am sure there are institutions that go against this law but I try to spread the word that Reg E doesn’t allow that practice.

https://www.washingtonpost.com/opinions/2024/01/24/cap-overdraft-fees-hurt-poor-families/#

Here’s the article.

plaintext

These people are far and away the heaviest users of bank overdrafts. The Financial Health Network, a personal finance nonprofit, says the group most likely to overdraft includes “financially vulnerable” households that struggle to pay their bills every month and typically make less than $30,000 a year. Almost half of financially vulnerable households with checking accounts overdrafted in 2022, and of that group, two-thirds overdrafted at least three times, one-third did so six or more times, and one-fifth overdrafted 10 times or more. With an average overdraft fee of $26.61, hundreds of dollars in fees can land on the most cash-strapped customers. Capping those fees — possibly as low as $3 — would be a huge boon to families who really need the help. Who could oppose that?

Well, as with any nice-sounding policy, it’s important to consider the alternatives, both for the customer and for the banker.

For depositors, overdraft fees can be an expensive alternative to even worse options, such as payday loans or having their electricity shut off (and paying a reconnection fee to turn it back on). And “the best of bad alternatives” can also be sort of true for bankers, who must find some way to defray the cost of providing what is basically an unsecured loan to people who are, as we’ve seen, often financially struggling and might be unable to repay the money. The fees also help pay for “free” checking (which costs banks quite a bit of money to provide).

If we cap overdraft fees, how will banks make up the lost revenue?

From profits, you say, and fair enough, but Patrick McKenzie, who writes the Bits About Money newsletter, points out that the reason your bank is so obsessed with getting you to sign up for paperless statements is that the profit margins on checking accounts are so thin, they can be meaningfully improved by saving the cost of 12 stamps a year. “Margins on small bank accounts are very thin,” he wrote recently, and “credit losses can easily be larger than several years of them.”

Now the government wants to make those accounts even less profitable. It seems possible banks would look to limit their losses by getting rid of those customers or making up the revenue somewhere else — or possibly both. This seems to have happened in the past, judging from what we saw when federal regulators preempted some state fee caps in 2001. According to researchers from the New York Fed, the exempted banks both raised overdraft fees and expanded available overdraft credit, while lowering minimum balance requirements. The rate at which checks were returned for insufficient funds declined by 15 percent. And the share of low-income households with a bank account rose by 10 percent, suggesting that minimum balance requirements had kept those households from opening accounts.

That doesn’t mean that no one would benefit from this rule. High overdraft fees can also deter people from opening a bank account, and it’s possible that effect would outweigh any contraction of credit. The financial industry has also changed a lot since 2001, with nonbank alternatives, such as Cash App, that might offer the marginal bank customer a better replacement than an old-fashioned check-cashing store. But there would still likely be winners and losers, and I don’t know whether the former’s gains would outweigh the latter’s losses. I’m not sure the administration does, either.

Won’t somebody think of the bankers! They hardly make any money at all on your broke ass $16.42 balance account!

it’s only a problem if you see the banks as only a profit source and not as a service.

We had to force corps / government to give us days off, Healthcare, voting, not being slaves, electricity, water, internet… all things they wanted to be products and not services

Yeah, you don’t make a huge amount of money on a service that everyone needs - boo fucking hoo, close the business and get a real job and stop eating avocado toast.

“You start nailing one white banker per week to a big wooden cross, you’re going to see that drug traffic begin to slow down pretty fucking quick.”

What’s this from?

Carlin

Truly one of the dumbest articles that I have seen.

Having any margin at all on a checking account is just gravy for a bank. It is not their primary source of revenue and never has been. Checking accounts are a mechanism to get customers to do business with them. It’s a marketing/advertising program, that has become required in the industry.

Bank’s are only interested in loans and deposits. This is where banks make the bulk of their money.

When it comes to the poorest people in society, they are not depositing much money or taking out loans. Bankers see them as freeloaders on a system designed to draw in people with more money. They can’t outright deny to service them without a marketing disaster so they punish them instead. Taking money from them to help defray the cost of their marketing efforts. Instead of just denying the charge for insufficient funds as they ethically should, they created an elaborate fee system to bleed money from them.

This is why you should always deny the overdraft protection on any checking account. Never let them charge you a fee for a charge they should have rejected.

If banks lose profit, they leave that customer group.

I always wonder why it is like a given that they have to make a certain amount each year or else. What would be so bad if they just made a little less?

I think I killed some brain cells reading this article, but I’m glad you posted it, thank you!

No problem.

Paywalled. Open in incognito.

Their point is that poor people use overdrafting instead of making actual loans. Removing the overdraft revenue from banks would make banks not offer it, making it necessary for poor people to take worse loans.

It’s just an opinion piece and the author admits that it could have other results.

The general concern is if you remove the overdraft fee as a tool, banks will just require a minimum or cancel you.

If financially struggling families can’t even access basic banking, they are further disenfranchised and removed from a stability, and eventually wealth generation

Sounds like a great time to actually bring back postal banking if the “job creators” can’t handle just making “some money” instead of " lots of money" from these accounts.

I’m sure the post office would be glad to have the “some money.”

Well under Obama there was that weird sorta savings account thing they had. I dropped twenty bucks in it just to check it out. They ended the program I think in 2014.

Sounds fine. And unfortunately banks are extremely real job creators. The existence of loaned capital to start business, pay employees and so on are a course of business development.

Ultimately, weather you like them or not, you can’t force a business to work with a given customer, especially if that customer is unreliable or requires more work.

I agree the time of government is to look after people with less/no concern for their profitability, especially when basic well-being and stability are in play.

Yeah you can force a business to work with a customer they don’t want. Go open a restaurant and refuse to serve people based on race, see what happens. We force insurance companies to cover people with massive health problems, companies to make diversity hires, banks to lend money to minorities, buses to take pretty much anyone with a valid ticket, bakers to make gay wedding cakes…

Some how some way the world hasnt collapsed into ruin.

Obviously I’m not discussing a protected class.

As in, protected by law. No law exists currently to protect people with a low balance at a bank.

I more assume “banks will stop offering services if they make less” or “those hard limits teach you to not go below 0” which are dumb

Ugh I feel dirty for reading the article but the argument is your first option: “limit bank profits and they’ll stop doing business with poor people.”

Credit Unions is the answer if anyone actually believed this could even be slightly possible.

Yes. It’s exactly that.

deleted by creator