{kind=link}

I installed NetGuard about a month ago and blocked all internet to apps, unless they’re on a whitelist. No notifications from this particular system app (that can’t be disabled) until recently when it started making internet connection requests to google servers. Does anyone know when this became a thing?

Edit 2: I bought my Pixel 6 phone outright, directly from Google’s Australian store. I have no creditors.

Were the courts not enough control for creditors? Since when are they allowed to lock you out of your purchased property without a court order?

I don’t even live in the US, so what the actual fuck?

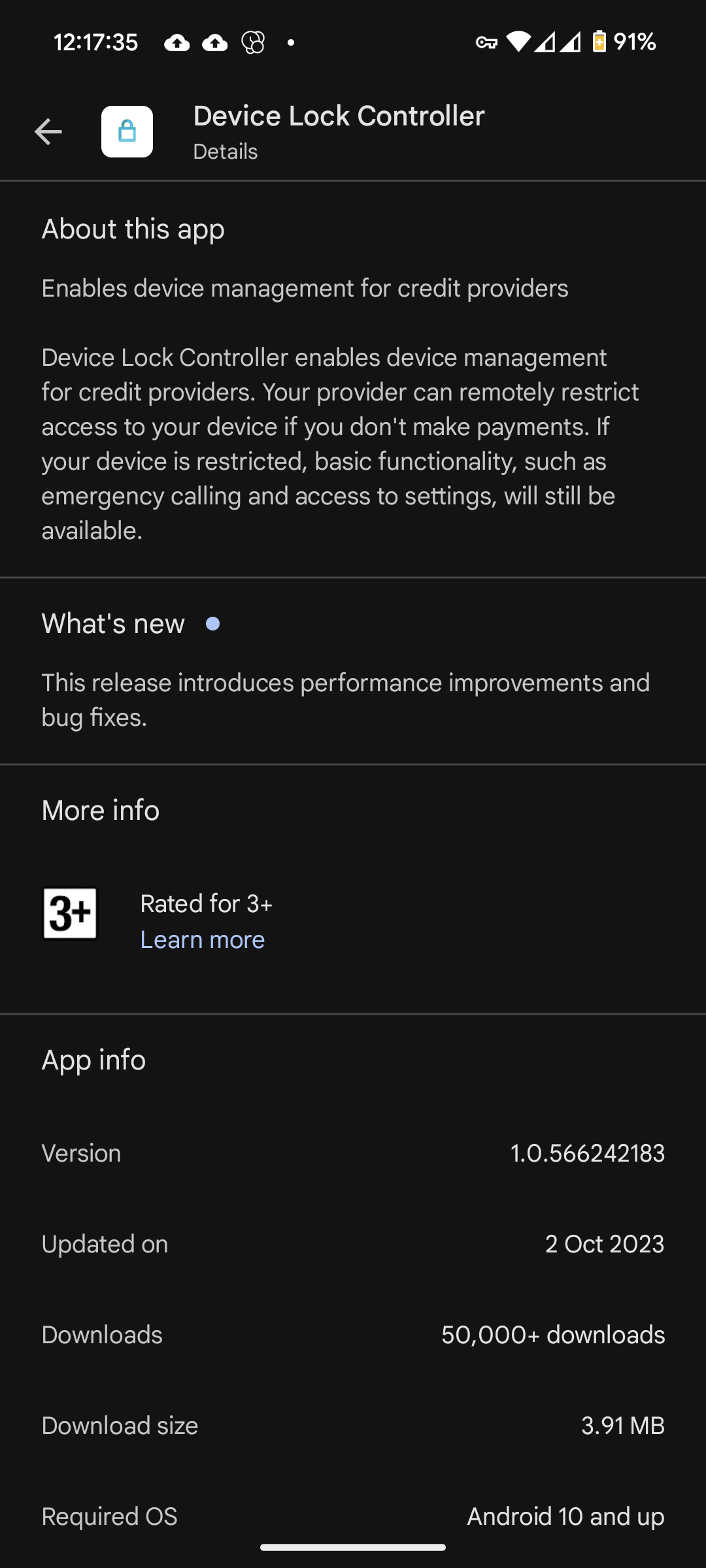

Edit 1: You can check it’s installed (stock Pixel 6 android 14) Settings > Apps > All Apps > three dot menu, Show system > search “DeviceLockController”.

I highly recommend getting NetGuard, you can enable pro features via their website if you have the APK for as low as 0.10€, but donate more, because it’s amazing. You can also purchase via Google Play store.

I know this is a privacy community, but I’m not sure I’m onboard with the outrage on this particular one. If you rent/lease or go on a payment plan for the device you’re using, then it isn’t yours, it belongs to the entity you borrowed it from.

If I don’t make car payments, the bank can repossess my ride. If I dont pay my mortgage or rent, I can be evicted by my landlord or bank.

If I don’t make my phone payment, the company should have recourse to prevent me from using their device.

This could open up the ability for bad actors to disable my device, and I agree that’s a horrible prospect. But the idea of a legitimate creditor using this feature to reclaim their property is not something I find shocking.

All your points are sound. The issue that I have with this is that remote disable functionality is not necessary to achieve any of these aims. Before they were connected to the internet, people were still able to rent/lease autos and the world managed to survive just fine. There were other ways for lenders to get remunerated for breaking lease terms - they could issue an additional charge, get a court order for repossession, etc. Remote disable was never needed or warranted.

So let’s start by considering the due process here. Before, there was some sort of process involved in the repossession act. With remote disable however, the lender can act as judge, jury and executioner so to speak - that party can unilaterally disable the device with no oversight. And if the lender is in the wrong, there is likely no recourse. Another potential issue here is that the lender can change the terms at any time - it can arbitrarily decide that it doesn’t like what you’re doing with the device, decide you’re in breach, and hit that remote kill switch. A lot of these things could technically happen before too, but the barriers have been dramatically lowered now.

On top of this, there are great privacy concerns as well. What kinds of additional information does the lender have? What right do they have to things like our location, our habits, when we use it, and all of the other personal details that they can infer from programs like this?

There are probably lots of other issues here, but another part of the problem is that we can’t even start to imagine what kinds of nefarious behaviors they can execute with this new information and power. We are well into the age where our devices are becoming our enemies instead of our advocates. I shudder to think what the world would look like 20 years from now if this kind of behavior isn’t stopped.

Perfectly stated! The moralizing story kind of serves as cover, as a complete blank check to excuse practically any behavior of the lender, without any limiting principle.

Right - they say that they’re just going to use it to defend their “property rights”. In practice, they’re going to use it for a whole lot more than just that…

Exactly. These types of changes grant corporations extrajudicial power.

I don’t disagree with anything you say. I think it’s worth mentioning that the cost of enforcement directly informs the cost of a lease/rental situation. The cheaper they can enforce the contract, the less they can theoretically charge. If they had to get a court order to lock your phone or repo your car, they’d make it more expensive or be much more selective about who they lease/rent to. This maybe enables more people to have phones or get cars?

I swear I’m not rooting for team “aggressive manipulative business behavior widens opportunities for the less well off”. Gross. Kind of how I hear about globalization of manufacturing stuff - “they get paid pennies!” “yeah, but that’s more than before the factory came? look what they can buy now” I know that’s a overly broad generalization but you see those arguments.

Of course! I hope you didn’t read my comment as hostile. I read yours as sort of a devil’s advocate type of argument and was just trying to point out the logical flaws in it. I’m glad that you didn’t hesitate to voice a contrary opinion. The points that you raise are interesting… and it’s always good to consider both sides of the argument, even because it just helps us hone our own arguments. You could certainly argue that this is just another enforcement mechanism. It’s just that it comes with a lot of unintended consequences, which most people will overlook, and they’ll inevitably be used in ways that we didn’t anticipate, long after the fact that these kinds of mechanisms become commonplace.

Regarding the reduced cost of lending: sure, in theory they could lower the prices. In practicality, will it? Any time we see cost-reducing developments, it usually ends up resulting in higher profits for the vendors moreso than better competition and lower prices for consumers. Look at how car manufacturers are just letting electric vehicles sit in their lots because they refuse to accept what buyers are willing to pay. The corporate types really, really hate to lower prices on anything for any reason. So I would be surprised to see something like that happen, even though it’s still theoretically possible…

Oh nono no, the world is much worse than that:

If you make all your car payments on time except one, the bank can still repossess your car.

If you pay your mortgage or rent on time every time except once, the bank can initiate the process of eviction.

Remember: the power triangle points down

I paid off a car without ever being late, and they reported my account as unpaid and in collections at the end. They had no reason to do so and to this day I still don’t understand why they did it. I contested it and the best I was able to accomplish was getting the entire loan removed from my credit report. So 2 entire years of on-time payments and satisfactory completion of a loan resulted in no positive credit boost for me, and a big PITA, just because the company made a mistake. Companies are not responsible enough to wield the type of power that this app grants.

Yes? That’s why loans with collateral charge a lower interest rate than unsecured loans.

My point being that if said bank screws up whilst dealing with your loan, and you make a fuss to hold them accountable, the worse thing that happens to them is that they issue an apology.

Not an unreasonable thought, but my question is what is the process to disable? In your examples, there are legal steps/requirements to repossess those assets.

In this case I can’t imagine the process is longer than “press the brick button and extort money”

Is it extortion if it’s contractually obliged?

¯_(ツ)_/¯ eye of the beholder I suppose

That’s not how it works, at least in Spain.

I agree completely, but it’s an odd way to go about repossession.

And there’s the rub. Sure, it’s a financed phone. It doesn’t follow that we have to suspend judgment on the means they resort to, to enforce their terms.

I find it funny how differently Lemmy reacts to something like this vs reddit. The Lemmy community is certainly very different than reddit.

https://www.reddit.com/r/Android/comments/jpdup2/google_app_lets_banks_lock_your_phone_if_you_dont/

What about for people like me?

I bought my device outright. No loans, no payment plans and no reason for that functionality to exist on my phone. Yet there it is, just waiting to be taken advantage of whether there is a valid reason or not.

This is the kind of apathy that leads to phrases like, “If only we had known” but we do … and do nothing about it.

I can and will at least do my part for myself and encourage others to do the same.

When I saw this on a custom ROM, it was basically the same thing, but said that my financial institution or whoever had admin access to my phone, including seeing texts and everything else, until my phone was paid off. Still not sure why that was there in a custom ROM, but I ended up not using it.

For every single one of those scenarios, a set of legal processes need to be exhausted. This app gives the lender the ability to do whatever they want, whenever they want, without following a set of legal processes.

That’s dystopian mentality at it’s greatest.

-Cory Doctorow from his blog, unintentionally addressing you